The S&P 500 index experienced a notable rebound from its monthly lows as investor sentiment improved, despite lingering uncertainties in the macroeconomic and geopolitical landscape. This upward movement occurred without a clear catalyst, as the market continues to trade within a range constrained by various risks. Notably, the US Supreme Court’s ruling on tariffs has created short-term uncertainty, although former President Donald Trump quickly responded by imposing new tariffs under different legal provisions. This shift reduces the effective average tariff rate, which could provide marginal benefits.

As the Federal Reserve considers its interest rate strategy, market participants are currently pricing in approximately 54 basis points of easing by the end of the year. This outlook may be subject to reevaluation should further positive data emerge from the US labour market. Federal Reserve Governor Christopher Waller indicated a preference for maintaining steady rates if the upcoming employment data mirrors the strong figures reported in January’s Non-Farm Payrolls (NFP) report. Consequently, the market will closely monitor data releases next Friday, as favorable outcomes could lead to a hawkish repricing that affects market dynamics.

The ongoing military tensions between the US and Iran represent another significant risk factor. An escalation into military conflict could trigger a spike in oil prices, posing a negative shock to the global economy and increasing the likelihood of stagflation. Initial market reactions would likely include heightened risk aversion, potentially leading to a selloff in the stock market and negative growth expectations.

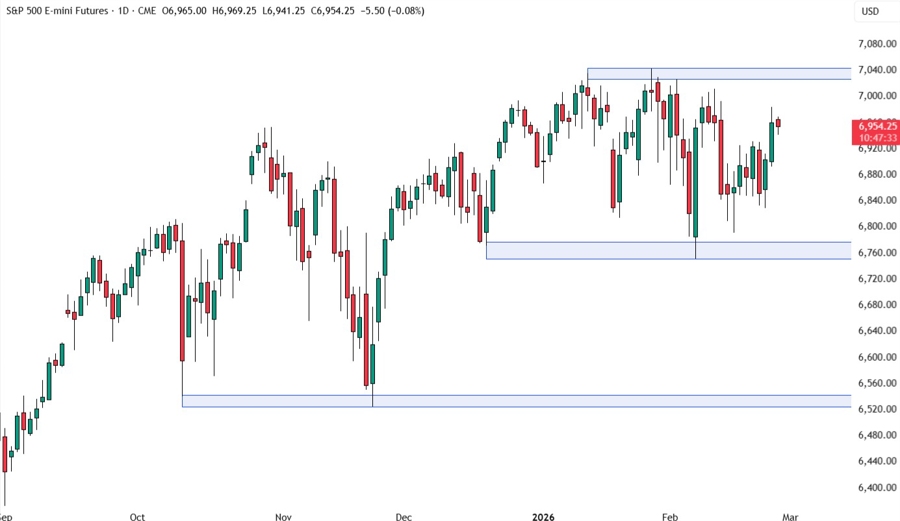

Despite these concerns, the macroeconomic environment remains relatively positive, driven by easing inflation and a strengthening labour market. Traders are advised to proceed cautiously, as the situation could shift rapidly. Currently, the S&P 500 is approaching its all-time highs after bouncing back from recent lows, and should it reach these peaks, sellers might enter the market to position for a downturn toward the 6,760 support level.

On the daily chart, the index’s trajectory indicates a potential challenge at record highs, where sellers may seek to establish positions. Conversely, buyers will be looking for a breakout above these levels to enhance bullish bets. The 4-hour chart shows robust support around the 6,930 level. Should the market pull back, buyers are likely to step in at this support with clearly defined risk parameters, while sellers will aim for a break lower to target the 6,760 support level.

For the 1-hour chart, the focus remains on the support zone, which offers a favorable risk-to-reward setup for buyers. Sellers, however, will require a decisive break lower to trigger further declines toward 6,760.

As the trading week progresses, market participants will be keeping a close eye on key data releases, including the third round of US-Iran talks and the US Jobless Claims data today. The week will conclude with the release of the US Producer Price Index (PPI) report tomorrow, which could further influence market sentiment and direction.