Global shipments of smart glasses surged by an impressive **139%** year-on-year in the second half of **2025**, according to data from **Counterpoint Research**. This growth is largely attributed to the rising popularity of AI-enabled glasses, which comprised **88%** of total shipments during this period. The market’s expansion is primarily driven by **Meta’s** dominance and a series of new product launches from various Chinese manufacturers.

The landscape for smart glasses has transformed significantly since **2023**, evolving from a niche curiosity to a burgeoning consumer electronics segment. Meta, in particular, has solidified its market position, commanding **82%** of shipments in the latter half of the year, an increase from its established dominance since the successful launch of the Ray-Ban Meta collaboration.

Meta’s Dominance and Product Expansion

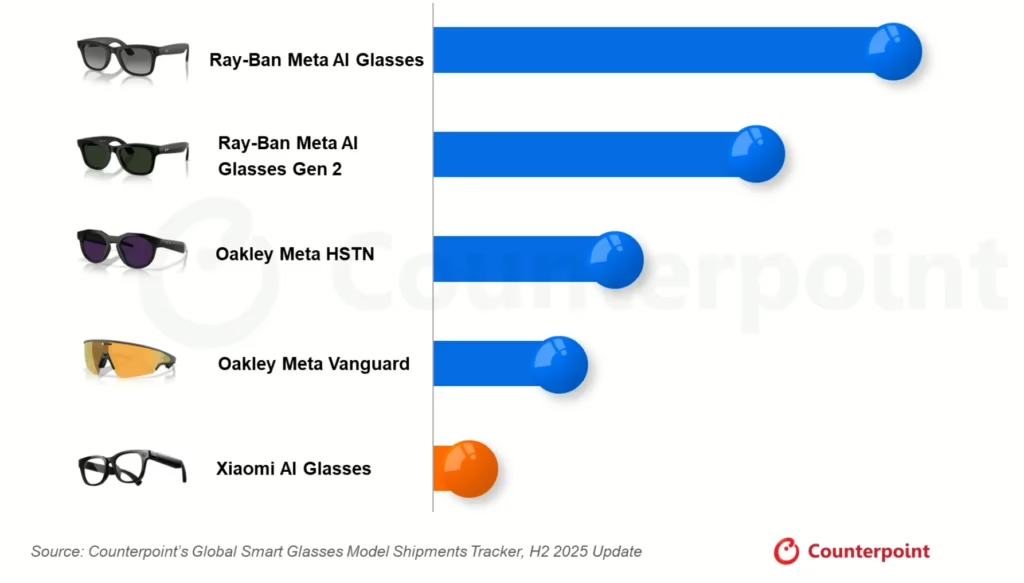

Meta’s robust market share reflects a multifaceted approach to product development. The company saw peak shipments of the original **Ray-Ban Meta AI Glasses** in the third quarter of **2025**, driven by seasonal demand. Additionally, the introduction of the second-generation model in **September 2025** garnered significant early traction. Notably, Meta’s sports-oriented products, including the **Oakley Meta HSTN** and **Oakley Meta Vanguard**, accounted for over **30%** of the company’s total shipments in the fourth quarter of **2025**.

Consumer feedback on the second-generation Ray-Ban model highlighted substantial enhancements in video performance, with improvements like higher resolution moving from **1080p to 3K**, expanded frame rate options, and upgraded features such as hyperlapse and slow-motion shooting. Despite these advancements, users consistently identified battery life as an area needing attention, a challenge that persists across the smart glasses category.

Market Dynamics and Pricing Trends

The pricing landscape for smart glasses in the second half of **2025** reveals a significant trend towards bifurcation. The average selling price (ASP) for AI smart glasses rose to approximately **$360**, up from **$347** in the first half of the year. This increase is largely driven by Meta’s premium positioning. Conversely, basic smart glasses experienced a sharp decline in ASP, dropping to around **$63** as consumer preferences shifted toward entry-level models from smaller manufacturers like **OHO Sunshine**.

This division in the market impacts the display and optics supply chain. AI glasses, with an ASP of **$360**, justify higher investment in components such as embedded displays and advanced cameras. In contrast, the under **$50** segment is increasingly commoditized, primarily serving as audio accessories with added visual components.

Regional dynamics also play a crucial role in market growth. North America remains the largest market, capturing **37%** of global shipments. However, Western Europe demonstrated notable growth, surging to **30%** of the market, fueled by new product launches from Meta. **India** experienced remarkable expansion, with shipments increasing **15-fold** following Meta’s official market entry in May **2025**, although its overall share remains at just **2%** globally.

China’s market trajectory presents a more complex picture. While shipment volumes increased, the country’s share of global shipments fell to **6%** due to a plethora of products launched late in the year that shipped in limited quantities. **Xiaomi**, the leading Chinese manufacturer, ranked second globally after Meta, achieving over **200%** year-on-year shipment growth following the launch of its AI glasses in June **2025**.

Looking ahead, the competitive landscape may shift significantly if even a few of the numerous smaller Chinese OEMs manage to achieve meaningful volume in **2026**.

Future Challenges and Component Costs

Despite the impressive growth, challenges loom on the horizon. Counterpoint Research notes that rising memory prices could pose difficulties for AI glasses in **2026**. However, the firm suggests that the impact may be limited due to the high gross margins currently enjoyed by AI glasses, alongside the relatively small proportion of memory in the overall bill of materials.

As the market continues to expand into lower price tiers, this dynamic could shift. The situation mirrors trends in the television market, where increasing component costs disproportionately affect brands competing on price rather than those positioned as premium.

In conclusion, the smart glasses market has demonstrated remarkable growth in the latter half of **2025**, with Meta firmly at the forefront. As the industry evolves, it will be essential to monitor how pricing dynamics, regional developments, and competition from emerging manufacturers shape the future of this technology sector.